Financial News vs. Noise

Jim Cramer VS Technical Analysis

I made a point in yesterday’s note that I think is extremely important. The Fed was wrong about inflation being transitory, and they are currently wrong about policy being restrictive. Both mistakes led to policy being overly accommodative. So while some of yesterday’s rally was due to a relatively cool PPI, I also think investors are brushing off sticky inflation based on an expectation that the Fed is going to ease anyway. Reading that the Magnificent 7 accounted for 95% of the S&P 500 gain. Don’t think this is bullish as those names are used as a flight to safety.

Not happy about the rise in yields either

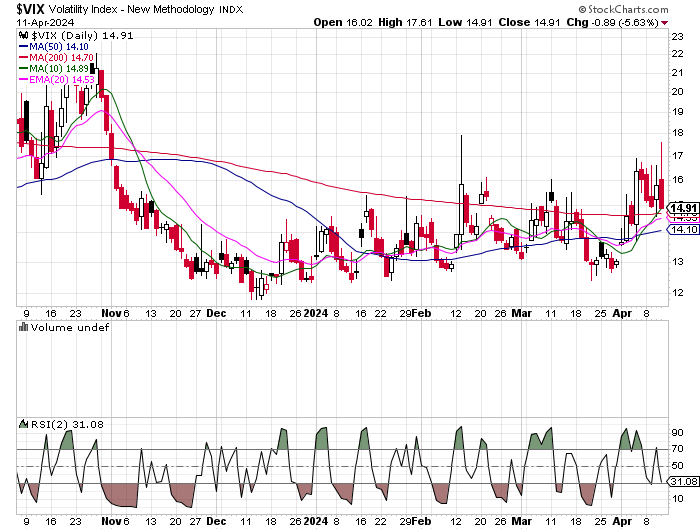

But do like to see this, VIX spiked only to end up at the lows

Remember though VIX needs a reason to stay elevated. I put much more stock in rates and the fact that yesterday was more about a rotation back into Mag 7 than it was a broad based rally. Seeing a lot of people all bulled up, maybe they are right, but I’d be a bit more cautious here. Big bank earnings today, so that could impact the narrative.

WSJ makes a great point here. Interest rate cut expectations have been going down, but perhaps they are being replaced by higher earnings expectations. Interest Rates Have Investors Worried. Profits Give Them Comfort.-WSJ

Stronger-than-expected economy portends fewer rate cuts this year and improving earnings

This could also be an issue. Iranian Attack Expected on Israel in Next Two Days-WSJ

Hard to see how a direct attack on Israel doesn’t lead to a much broader war in the Middle East.

Bottom line you still need to be buying the dips, but I suspect earnings season has to deliver.

Subscribe to our other newsletters

Laffer Tengler Research Bulletin

Matthew Tuttle is the Chief Executive Officer and Chief Investment Officer of Tuttle Capital Management, LLC.

At Tuttle Capital Management (“TCM”), we want to help educate investors about different ways to allocate and manage assets. TCM strives to create innovative portfolio management tools coupled with investment strategies designed to help mitigate risks and potentially enhance returns.

The views and opinions expressed herein are those of the Chief Executive Officer and Portfolio Manager for Tuttle Capital Management (TCM) and are subject to change without notice. The data and information provided is derived from sources deemed to be reliable but we cannot guarantee its accuracy. Investing in securities is subject to risk including the possible loss of principal. Trade notifications are for informational purposes only. TCM offers fully transparent ETFs and provides trade information for all actively managed ETFs. TCM's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. Trade notification files are not provided until full trade execution at the end of a trading day. The time stamp of the email is the time of file upload and not necessarily the exact time of the trades.

Tuttle Capital Management is not a commodity trading advisor and content provided regarding commodity interests is for informational purposes only and should not be construed as a recommendation. Investment recommendations for any securities or product may be made only after a comprehensive suitability review of the investor’s financial situation.

© 2023 Tuttle Capital Management LLC (TCM). TCM is a SEC-Registered Investment Adviser. All rights reserved.