Financial News vs. Noise

Breadth continues to be awful. According to Mike O’Rourke at Jones more than 100% of the S&P 500 gain for the week was due to NVDA, AAPL, AVGO, and MSFT.

It’s both. The fact that the Fed’s next move is a cut is enough to get investors comfortable that the Fed put is back. Big Tech — not the Fed — is driving the stock-market rally. Here’s what investors need to know.-MarketWatch

If you just look at the S&P 500 and NASDAQ then it’s clear we are in a rip roaring bull market. However, if you look at the Dow and Small Caps then it looks completely different.

As Nvidia soars, the stock market’s deflated laggards spark concern-MarketWatch

But outside a handful of megacap winners, the market is struggling. That handful of heavyweight winners account for a growing share of winners in the market-cap weighted S&P 500 index SPX and Nasdaq Composite COMP. The S&P 500 has rallied another 2.9% so far in June, bringing its year-to-date gain to 13.9%.

The equalweight version of the S&P 500, which as the name implies gives the same weighting to each of its components, is down 0.4% in June and has gained just 4.4% year to date. The more cyclically oriented and, importantly, price-weighted Dow Jones Industrial Average DJIA also notably lags behind the cap-weighted indexes, down 0.3% in June and up just 2.4% in the year to date.

Keep an eye on this. Friday’s trading could trigger a $10 billion rush of demand for Nvidia shares. Here’s how-CNBC.com

At stake is one of the top two spots in the Technology Select Sector SPDR Fund (XLK), whose June rebalance is based on market cap values as of Friday’s close. Apple and Microsoft are the two biggest holdings in the fund, at roughly 22% each. Nvidia makes up less than 6% despite being only slightly behind the two leaders in market cap.

A lot of talk about why people are not more optimistic about the economy, my guess is all those people asking are rich. Inflation is widening the divide between how the wealthy and everyone else sees the economy-MarketWatch

A steadily growing economy and low unemployment have helped to ease some of the pain of high inflation, but middle- and low-income Americans say they are feeling more stress.

The latest evidence was a drop in the consumer sentiment index in June to a seventh-month low. The decline stemmed mostly from rising anxiety among middle-and lower-income Americans.

@Mayhem4Markets

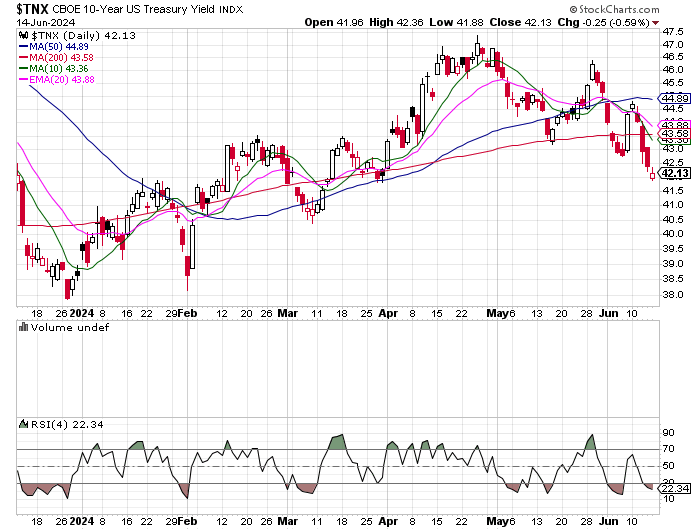

Regardless of a “hawkish” Fed statement, rates continue to come down. Perhaps the bond market is thinking that the economy is worse than the numbers show and traders figure the Fed is going to be forced to cut more aggressively?

Hate to be a broken record on regional banks, but KRE is getting close to the lows of the year while the S&P continues to make all time highs.

Precious metals and miners bounced back a bit. I can’t help but wonder if lower rates, banking sector weakness, and higher precious metals prices are telling us something.

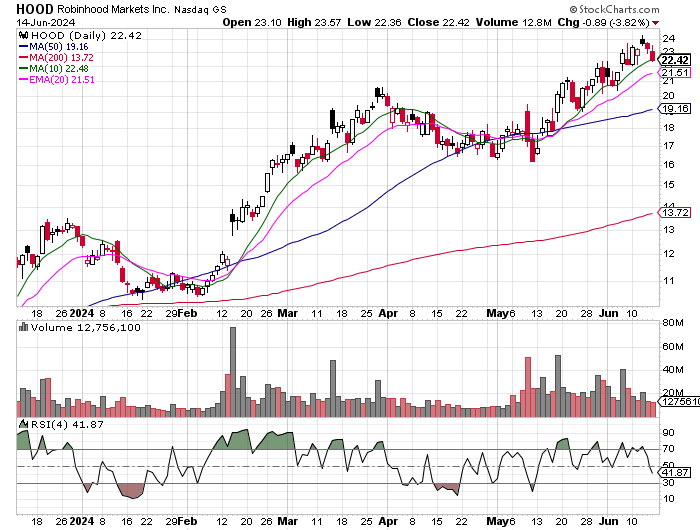

Nothing too interesting on our watchlist this morning. HOOD is a name we did pretty well with a couple of weeks back, will be looking to buy the any dip today.

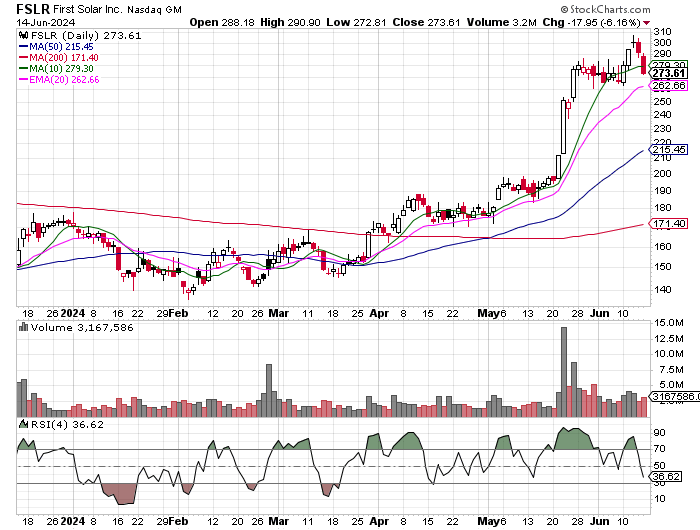

We were short FSLR last week and will be possibly looking to flip long today.

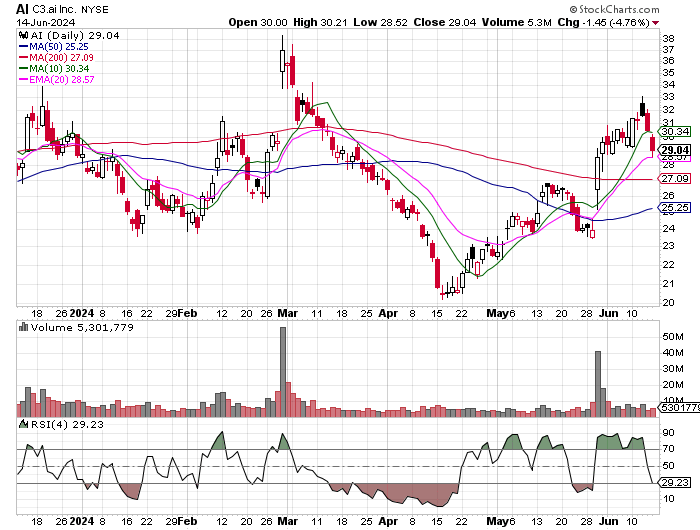

AI is another name we will be looking to buy the dip on.

Took profits on my Argentine positions on Friday. This is something to keep an eye on.

It was a familiar scene. For more than 30 years reformers have tried to end the destructive fiscal, regulatory and monetary policies that have made this once-prosperous nation poor. Partisan forces, mostly Peronist, have met repeated attempts at meaningful change with staunch resistance in Congress and mob violence in the public square.

Been taking a beating on my China positions lately, perhaps this is the start of a turnaround.

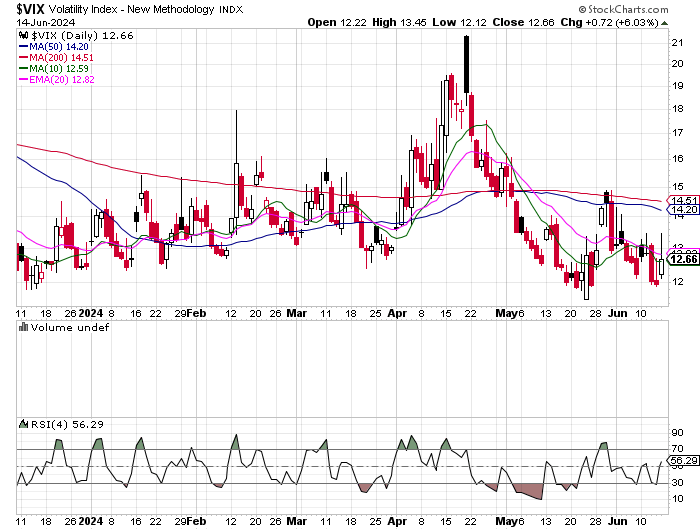

After Friday’s pop in VIX our models are all over the place. Our VIX spike models went short but some of our other models are still long. Looking at the chart would prefer some long VIX exposure here.

Count me in on this. Investors Fear Long Stretch of Calm in Markets Can’t Last-WSJ

Subscribe to our other newsletters

Laffer Tengler Research Bulletin

Matthew Tuttle is the Chief Executive Officer and Chief Investment Officer of Tuttle Capital Management, LLC.

At Tuttle Capital Management (“TCM”), we want to help educate investors about different ways to allocate and manage assets. TCM strives to create innovative portfolio management tools coupled with investment strategies designed to help mitigate risks and potentially enhance returns.

The views and opinions expressed herein are those of the Chief Executive Officer and Portfolio Manager for Tuttle Capital Management (TCM) and are subject to change without notice. The data and information provided is derived from sources deemed to be reliable but we cannot guarantee its accuracy. Investing in securities is subject to risk including the possible loss of principal. Trade notifications are for informational purposes only. TCM offers fully transparent ETFs and provides trade information for all actively managed ETFs. TCM's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. Trade notification files are not provided until full trade execution at the end of a trading day. The time stamp of the email is the time of file upload and not necessarily the exact time of the trades.

Tuttle Capital Management is not a commodity trading advisor and content provided regarding commodity interests is for informational purposes only and should not be construed as a recommendation. Investment recommendations for any securities or product may be made only after a comprehensive suitability review of the investor’s financial situation.

© 2024 Tuttle Capital Management LLC (TCM). TCM is a SEC-Registered Investment Adviser. All rights reserved.