Financial News vs. Noise

I am scheduled to be on Bloomberg today at 12:15 to talk about single stock ETFs. Going to be on Wolf_Financial spaces Thursday at 2pm to talk about our new 2x Bitcoin ETFs.

https://x.com/WOLF_Financial/status/1809986104394764594

Probably a perfect jobs number on Friday as far as the market is concerned. Strength this month, but previous month’s revised down. Gives the Fed cover to cut in September but doesn’t signal a recession.

S&P 500 scores record high as jobs data point to cooling ‘but not collapsing’ economy-MarketWatch

“The economy is cooling, but not collapsing,” said Andrew Slimmon, senior portfolio manager for U.S. equities at Morgan Stanley Investment Management, in a phone interview Friday. “The market is not pricing in anything more than a slowdown.”

Speaking of September, if Nickileaks is talking about it, pay attention.

Case for September Rate Cut Builds After Slower Jobs Data-WSJ

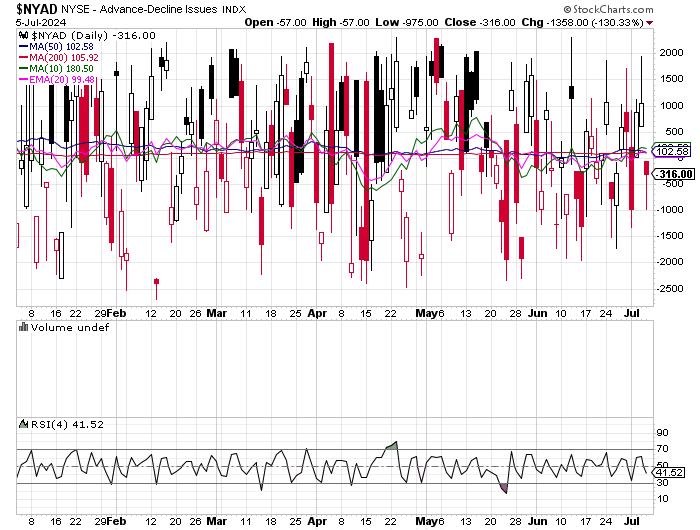

Risk assets seemed to like it. The market is starting to look very overbought here. I’ve been adding to shorts as my short watch list eclipses my long one these days. You don’t necessarily want to fight this trend, but I do think having some hedges is prudent. Breadth was not great on Friday, the percent of stocks above their 20 day moving averages ticked down.

As did the advance/decline line.

From Jonathan Krinsky…

In many ways this is an unprecedented market with few parallels. Sure we have seen periods with lopsided breadth (late '90s), optimistic sentiment (late '21) and low-volatility ('17). Yet the current market seems to have all of them, in some cases at extreme levels, and yet nothing seems to break the current cycle. What is clear is that the broadening we saw in late '23 on implied rate cuts is not happening this time around

Earnings Season to Test Investors’ Faith in Big Tech Stocks-WSJ

The growing size of the index’s heavyweights means a lot is riding on their ability to deliver profits and guidance in coming weeks that justify their sky-high valuations.

From Mike "O’Rourke on valuations and multiples..

The current behavior emulates that of Q1 2000. The market becomes comfortable with lofty valuations and then comparisons start. For example, the belief emerges that if Nvidia can trade 43x forward earnings, then the Blue Chips of the past two decades, Apple and Microsoft, should be able to support multiples in excess of 30x forward earnings and still be attractive. Technically, that is true in the short term, but paying high multiples for the largest companies in the stock market historically has not worked well. From 2000 through the end of 2020, Microsoft and Apple had registered median monthly P/E ratios of 20.7x and 19.1x earnings respectively. Last week's rally pushed Microsoft to more than 40x earnings and Apple to more than 35x. The fact remains that neither company is experiencing anywhere near the growth Nvidia has experienced over the past year. Although Nvidia is expected to continue that growth throughout this year, this is a megacap growth phase unlikely to be replicated in the foreseeable future by current public companies, including Nvidia. Thus, as they have done historically, multiples will contract again. As the companies with the lowest multiples in the Mag7, the rallies in Google and Meta Platforms are more understandable. Both companies trade approximately 28x trailing earnings and less than 25x forward earnings.

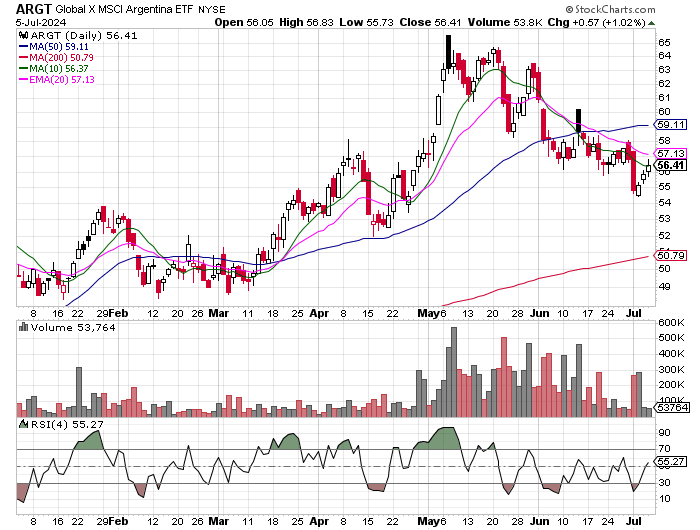

With an overbought market and continued bad breadth I would continue to look at this thematically. Look to buy dips on anything AI and AI infrastructure related, precious metals, law and order, and Argentina.

This week we have CPI and PPI along with Powell’s testimony to the House and Senate.

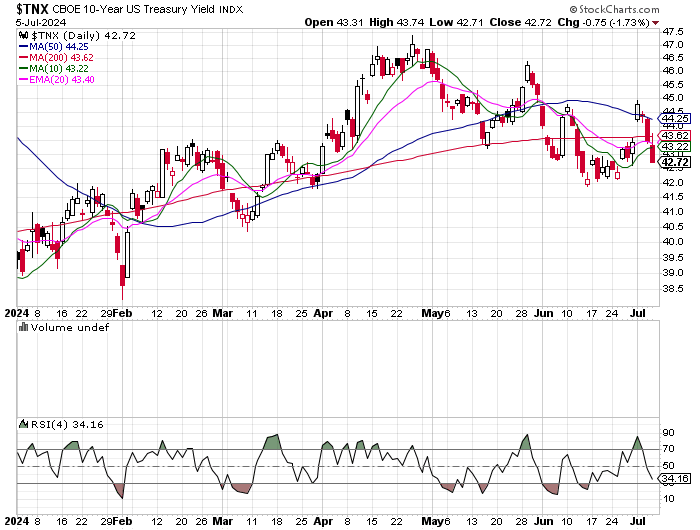

Rates continue to move down.

Looks like the 10 year wants to test the lows.

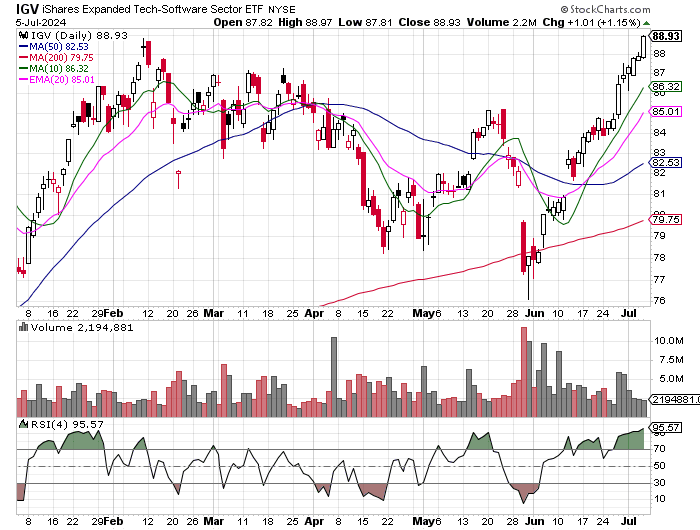

Software won’t quit.

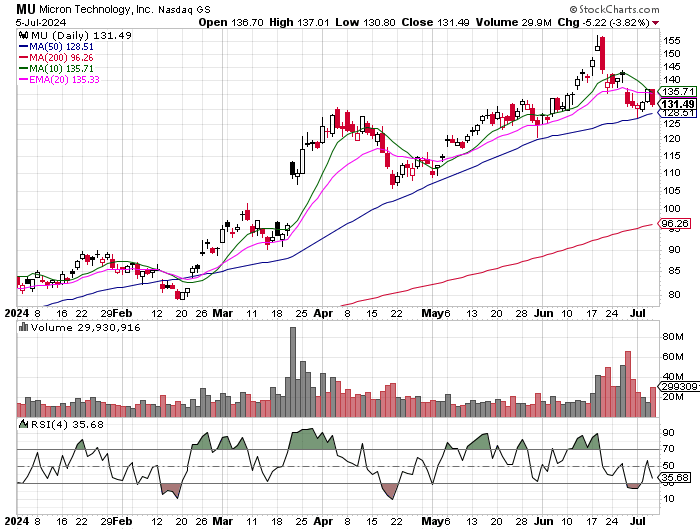

Semi’s are not as strong, but keep moving up, except MU.

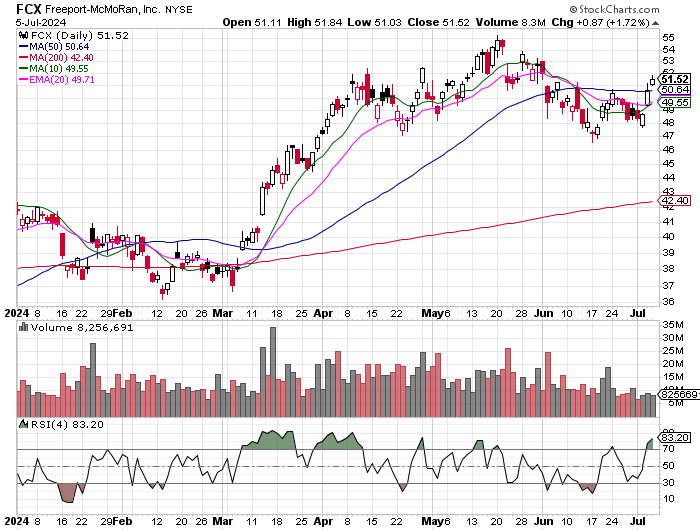

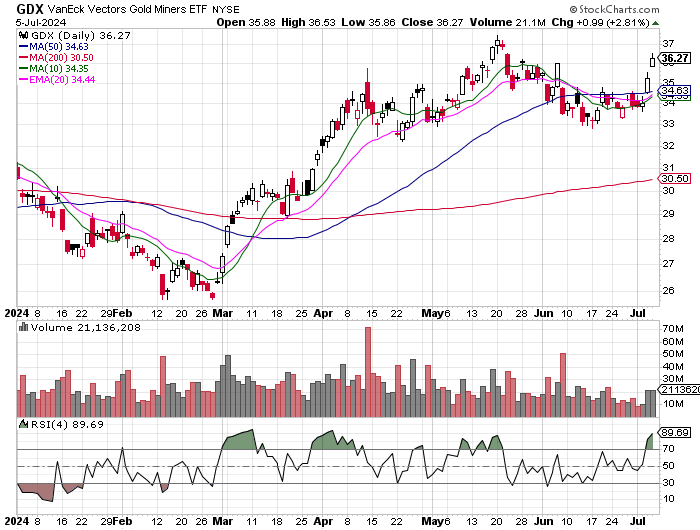

Precious and industrial metals continue to be strong.

This could be why. Hedge funds pile into commodity sensitive stocks at fastest pace in five months: Goldman data-MarketWatch

Hedge funds have now reversed course in a buying spree that has seen them plow into the materials and energy sectors via a flurry of long bets on firms in sub-sectors including oil, gas & consumable fuels, energy equipment & services, containers & packaging and mining & metals, the report said.

Silver beat gold, copper — and even the S&P 500 — in the second quarter. What’s next?-MarketWatch

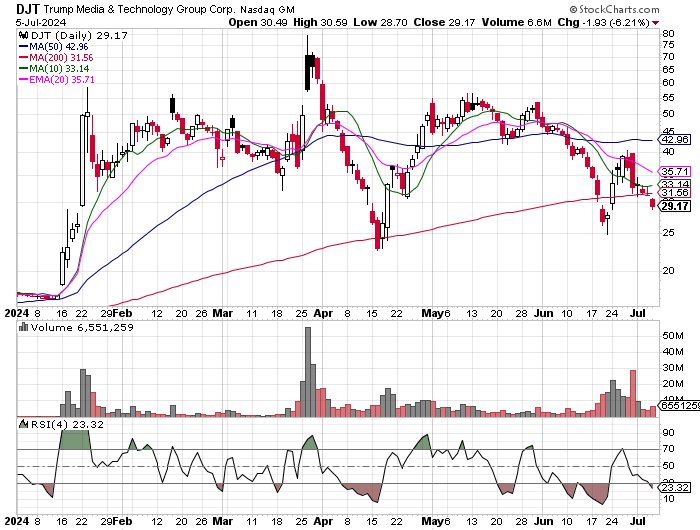

My law and order list (GEO, CXW, SWBI, and AXON) showed some weakness last week. I do think those stocks have more upside if Trump gets re elected and nothing happened last week that was bad for him. I haven’t been trading DJT lately but it seems to be moving in the opposite direction of the polls. If it re tests 25 it may be tempting.

The Argentine names were also weak, still would look to buy them on any dips.

Argentina’s Milei Has a Mixed Record So Far. He Still Needs to Tackle the Peso Problem.-Barron’s

Milei has made remarkable progress on Job No. 1, closing Argentina’s yawning fiscal gap, he argues. The treasury is running its first surplus since 2008, thanks to chainsaw-esque slashes to pensions, subsidies, and revenue sharing with regional governments. Inflation is falling fast, down from 25% monthly last December.

A lot of the energy names were weak on Friday, I would be looking to buy dips in them as well. That includes solar, coal, electric, and nuclear.

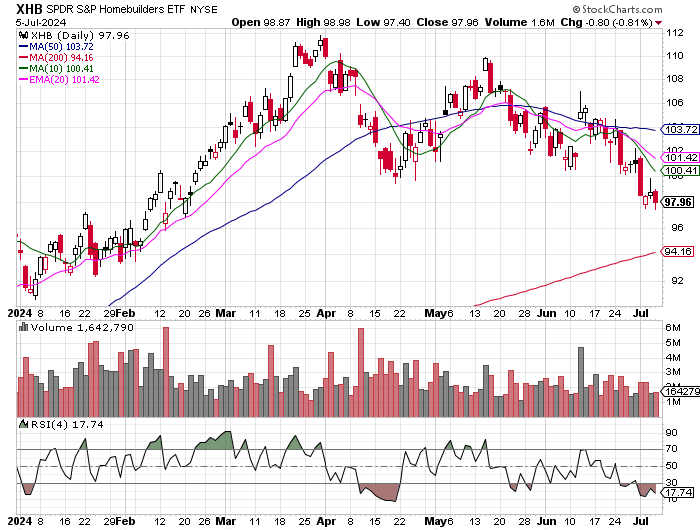

Homebuilders are interesting here as they have been declining at the same time as interest rates. This could be telling us something.

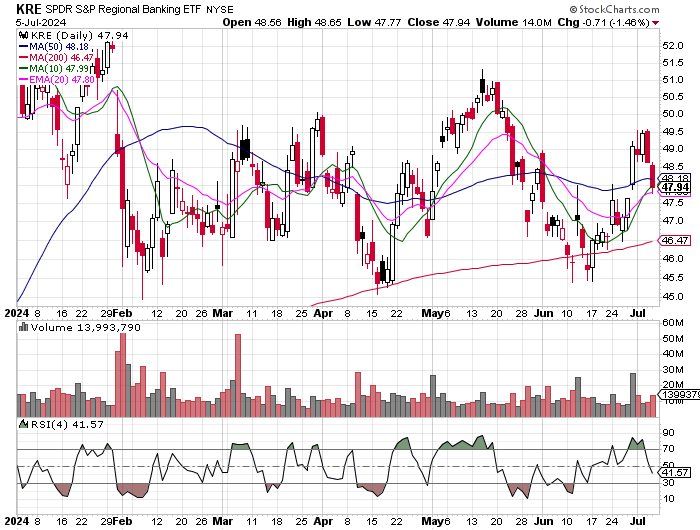

Same with the regional banks.

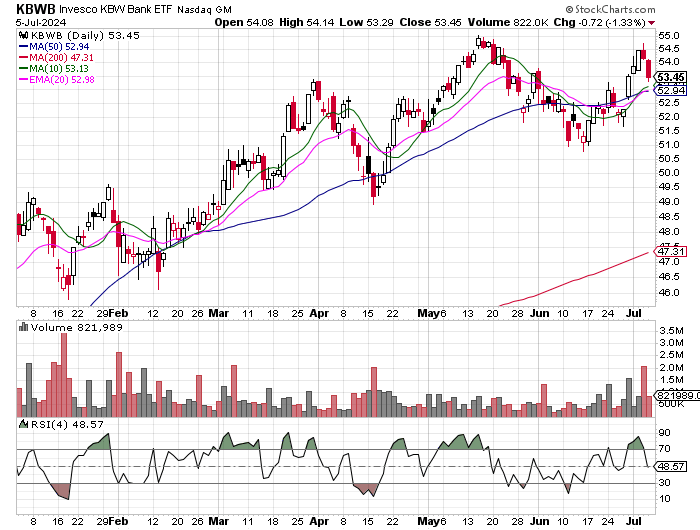

Then you have the big banks. Big Banks Are Taking Hits From Commercial Real Estate-WSJ

The trouble is at big banks and their loans to properties that are intended to be leased to third parties. For CRE loans involving properties that aren’t owner-occupied and are held by banks with over $100 billion in assets, more than 4.4% were delinquent or in nonaccrual status in the first quarter.

Looks double toppy….

Subscribe to our other newsletters

Laffer Tengler Research Bulletin

Matthew Tuttle is the Chief Executive Officer and Chief Investment Officer of Tuttle Capital Management, LLC.

At Tuttle Capital Management (“TCM”), we want to help educate investors about different ways to allocate and manage assets. TCM strives to create innovative portfolio management tools coupled with investment strategies designed to help mitigate risks and potentially enhance returns.

The views and opinions expressed herein are those of the Chief Executive Officer and Portfolio Manager for Tuttle Capital Management (TCM) and are subject to change without notice. The data and information provided is derived from sources deemed to be reliable but we cannot guarantee its accuracy. Investing in securities is subject to risk including the possible loss of principal. Trade notifications are for informational purposes only. TCM offers fully transparent ETFs and provides trade information for all actively managed ETFs. TCM's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. Trade notification files are not provided until full trade execution at the end of a trading day. The time stamp of the email is the time of file upload and not necessarily the exact time of the trades.

Tuttle Capital Management is not a commodity trading advisor and content provided regarding commodity interests is for informational purposes only and should not be construed as a recommendation. Investment recommendations for any securities or product may be made only after a comprehensive suitability review of the investor’s financial situation.

© 2024 Tuttle Capital Management LLC (TCM). TCM is a SEC-Registered Investment Adviser. All rights reserved.