Financial News vs. Noise

Not the way you want to see the market close, but so far so good this morning. Looks like the main culprit is this….

The whole idea of a Central Bank not doing what they think they need to do because market’s are unstable doesn’t make me bullish.

Interesting note on earnings season from Mike O’Rourke last night. All this focus on Japan and perhaps we lose focus on what’s most important here….

First, earnings season has underwhelmed and the Magnificent Seven have not bailed it out. The following data comes from Standard & Poor's. When earnings season started, the forecast was for year over year Q2 earnings growth of 5.7% and sequential growth of 6.2%. With approximately 60% of companies having reported, the year over year growth was 2.9% and sequential growth was 3.2%. The real kicker here is not Q2 softness, it is the back half of the year. As first half earnings grow low single digits, the forecast for second half earnings growth is 18%. It should be clear those estimates are not in the realm of reality, especially with a slowing economy. If earnings growth continues as the current first half pace, 2024 earnings growth will be approximately 4%. An equity market trading 23x to 25x earnings needs to do better than that. There is a lot of hope banking on Nvidia's report at month end.

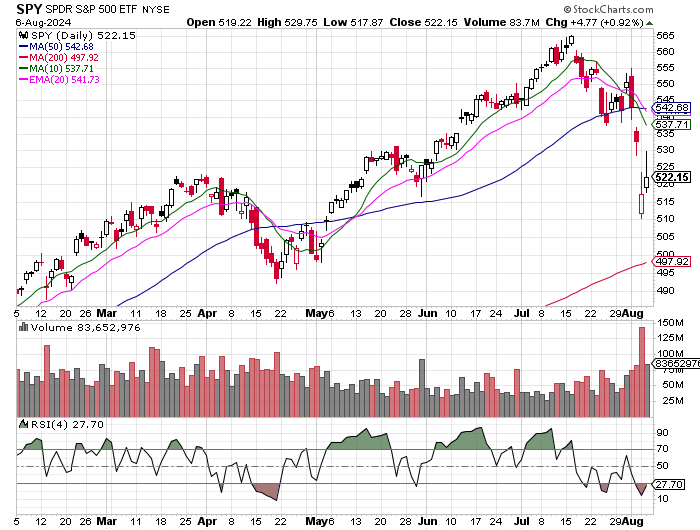

Would be watching Friday’s low ($528.60) on SPY for a possible undercut and rally move.

However, I am not yet ready to fully believe this bounce and would prefer the market to consolidate here a while. What I prefer often doesn’t matter though.

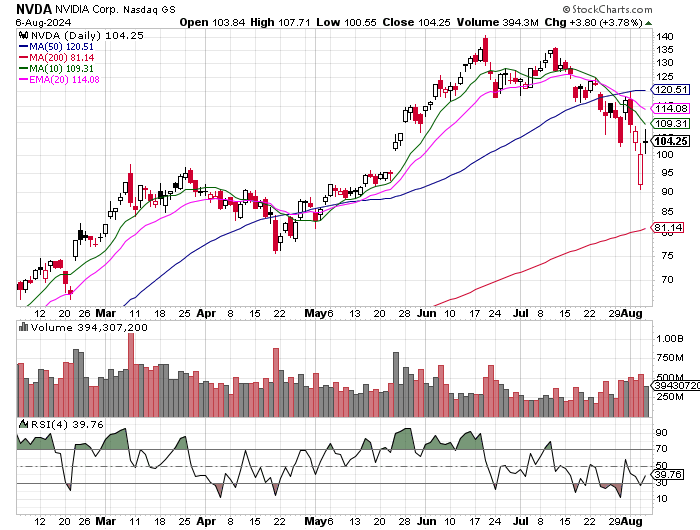

NVDA had a strange pop after hours yesterday, and so far this morning is keeping some of those gains. This looks to be the reason. Nvidia Stock Rising Again. How Super Micro Allayed AI Chip Fears.-Barron's

Super Micro CEO Charles Liang said a reported delay in shipments of Nvidia’s next-generation Blackwell chips wouldn’t impact his company much, noting there was a “normal possibility” of a delay when vendors introduce new technologies but the company would still be able to deliver its liquid-cooling solutions to its partners without much impact, in a call with analysts.

Couple of spots I would be watching here. Support at $100 obviously, but then $101.37, $101.51, and $102.54. Yesterday’s low of $100.55 also. To be bullish would love to see it break above yesterday’s high of $107.71 and Friday’s high of $108.72.

Still believe this is a problem that hasn’t fully shown itself yet. Are Banks Sweeping Dud Property Loans Under the Rug? New accounting rules should give investors an earlier warning, but surprises are cropping up and there could be more to come-WSJ

The pandemic sent office values in many big cities tumbling as more people worked from home. Now, for many borrowers, refinancing isn’t an option because the buildings are worth less than the borrowers owe. That makes defaults inevitable. Until then, though, the owners still may be current on their payments. Hope springs eternal, until it doesn’t.

C’mon. I’ve seen a lot of Black Swan events since I started trading in the early 80s, a 3% drop doesn’t qualify. Was the stock market’s 3% selloff Monday a ‘black swan’ event? Author Nassim Nicholas Taleb says no.-MarketWatch

This is interesting. It makes sense, short term interest rates are like 5% but most brokers pay little, if anything, on uninvested cash. SEC investigating Wall Street banks over ‘billions’ in lost interest payments-FT

Wonder how many of these are cash covered vs. on margin? The “smarter” way is cash covered. I occasionally sell puts, but only cash covered ones or as part of a calendar spread. Selling puts on margin can be picking up pennies in front of a steamroller. There’s a Smarter Way to ‘Buy the Dip’ Next Time-Barron's

Subscribe to our other newsletters

Laffer Tengler Research Bulletin

Matthew Tuttle is the Chief Executive Officer and Chief Investment Officer of Tuttle Capital Management, LLC.

At Tuttle Capital Management (“TCM”), we want to help educate investors about different ways to allocate and manage assets. TCM strives to create innovative portfolio management tools coupled with investment strategies designed to help mitigate risks and potentially enhance returns.

The views and opinions expressed herein are those of the Chief Executive Officer and Portfolio Manager for Tuttle Capital Management (TCM) and are subject to change without notice. The data and information provided is derived from sources deemed to be reliable but we cannot guarantee its accuracy. Investing in securities is subject to risk including the possible loss of principal. Trade notifications are for informational purposes only. TCM offers fully transparent ETFs and provides trade information for all actively managed ETFs. TCM's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. Trade notification files are not provided until full trade execution at the end of a trading day. The time stamp of the email is the time of file upload and not necessarily the exact time of the trades.

Tuttle Capital Management is not a commodity trading advisor and content provided regarding commodity interests is for informational purposes only and should not be construed as a recommendation. Investment recommendations for any securities or product may be made only after a comprehensive suitability review of the investor’s financial situation.

© 2024 Tuttle Capital Management LLC (TCM). TCM is a SEC-Registered Investment Adviser. All rights reserved.