Financial News vs. Noise

First big data point of the week was PPI, which came in cool. Today is CPI. The market now has a 90% probability on a 50 bp rate cut in September, so a hot number this morning could mess that up.

Bond Traders Look to US CPI to Buttress Half-Point Rate Cut Bets-Bloomberg

“I honestly think there’s compelling arguments on both sides,” Deutsche Bank’s chief US economist Matthew Luzzetti said on Bloomberg Television, referring to the debate over 25- or 50-basis-point cuts. “They are restrictive, the inflation data is telling them there’s not as much upside inflation risks. And then it depends on whether or not the economy is as resilient as we think.”

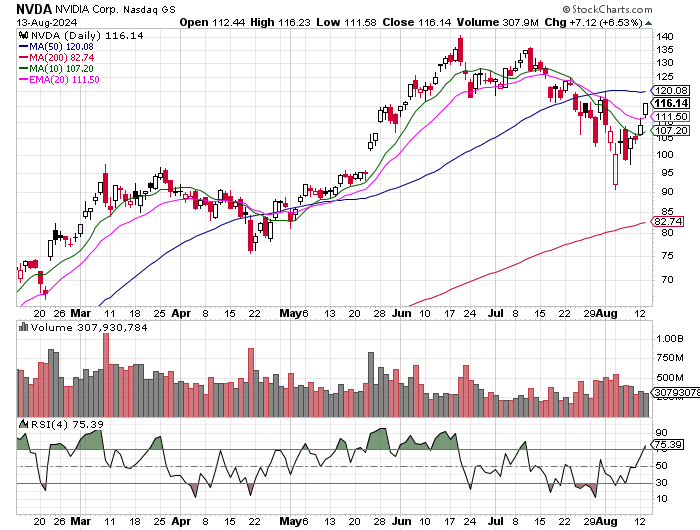

NVDA is up 10.9% in two days, with no real news out there. It has accounted for 36% of the gain in the S&P this week. After bouncing off the 90ish level it’s added almost 26 points. You still need to be buying the dips in NVDA.

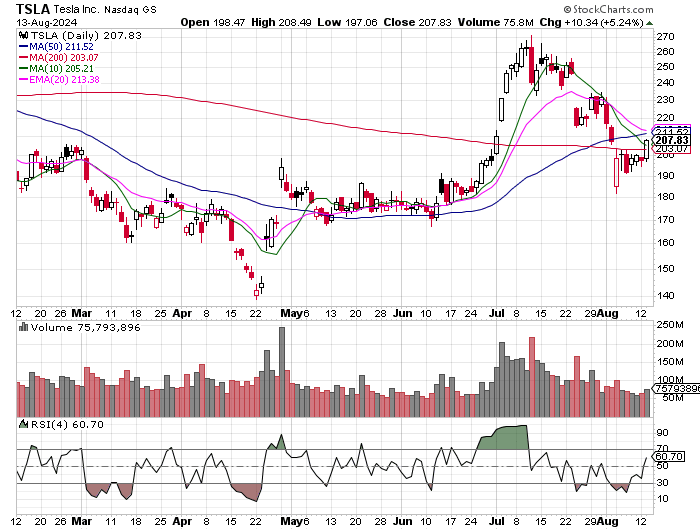

TSLA had an undercut and rally at it’s 200 day, which could be used as a long entry.

Same with AMZN and MSFT.

Collectively, the Magnificent 7 have been 66% of the gain in the S&P this week. META and AAPL look a bit extended, the other names all look pretty buyable here.

Overall the market looks short term overbought here. Our daily signal list has 5 longs and 25 shorts. Last time we got those types of numbers was near the top.

Interesting article this morning in the WSJ about AI. The Big Risk for the Market: Becoming an AI Echo Chamber-WSJ

AI-related corporations have significantly beaten analysts’ expectations, yet have lost 5% of their market value since the end of June. Part of this is because of an unwinding of trades using borrowed money, from which the market is already recovering.

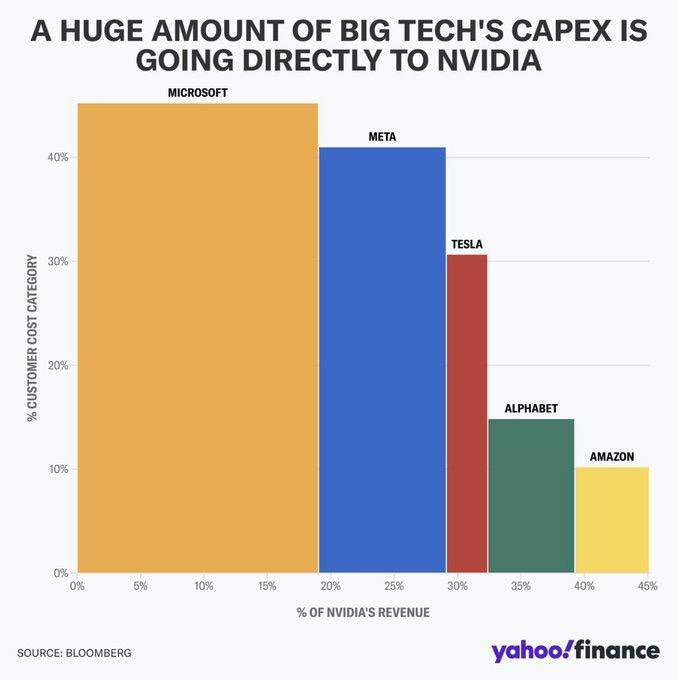

Higher up the supply chain, by contrast, are the “AI infrastructure” providers, which sell chips, data centers and training software. The undisputed leader is Nvidia, which has seen its sales triple in a year, but it includes other semiconductor firms such as Intel and Qualcomm, database developer Oracle and owners of data centers Equinix and Digital Realty.

Crucially, these latter companies are the ones that have delivered most of the upside for investors, by posting profit margins that are far above what analysts expected a year ago.

The important point, though, is that it is their role as ultimate developers of AI applications that have led them to make eye-watering capital expenditures, which are responsible for the profit surge in the rest of the ecosystem.

Annual earnings growth for these implementation-focused AI firms is likely to have slowed to around 22% in the second quarter, from a peak of roughly 50% last year. During the fourth, it is expected to come in at 8%.

Were it not for AI, revenues for semiconductor firms would probably have fallen during the second quarter, rather than rise 18%, according to S&P Global.