Financial News vs. Noise

The Watchlist will be live today around 11:30AM

https://youtube.com/live/Axs6UTldPto?feature=share

Somewhat interesting to see the VIX rallying a bit while the S&P 500 is also moving up. That usually doesn’t augur well for stocks. Could be traders hedging ahead of Jackson Hole, or more likely hedging ahead of Ueda.

BOJ’s Ueda Is Set to Face Intense Scrutiny After Market Chaos-Bloomberg

Either way, Friday is likely to be a big day. Depending on how my equity exposure looks I will most likely go into tomorrow with a good amount of SPY puts just in case. I have a way of trading them that makes them much less expensive, sometimes even free, so why not.

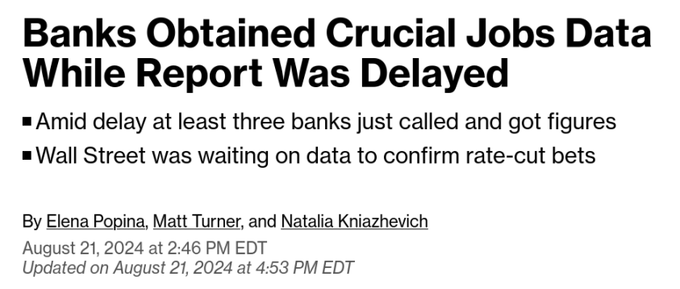

The big news of the day were the BLS revisions down 818k. The data was delayed and there were rumors that some banks got it before the rest of us did. Disappointing if true, but the data had zero market impact.

This is a bit frightening: Staggering Incompetence: Biden's Commerce Secretary Is "Not Familiar" With The Bureau Of Labor-ZeroHedge

We are too speechless to even offer any snarky, sarcastic commentary because, frankly, this is beyond idiotic.

Asked about today's near record downward jobs revision, Biden's Commerce Secretary Gina Raimondo - who we repeat, is the Secretary of the Department of Commerce which is responsible among other things, for the Bureau of Economic Analysis - said she "doesn't believe" the revision because, somehow Trump was behind it. But when she was informed that the data comes from her own administration, namely the Labor Department's Bureau of Labor Statistics, Raimondo's response was simply legendary: "I am not familiar with that."

FOMC minutes point to what we already know, cut in September. Jury still out on what size though. Market is pricing in 104bps for the year. Interesting take from Jefferies….

It is not obvious, in our view, if the minutes should be read as a positive for risky assets. While the readiness of the Fed to cut is a positive, the minutes also show increased concerns over the economy. Our read is that risky assets are in for greater volatility over the coming weeks as the market tries to decipher whether bad data is good news or bad news.

This is consistent with our models, which are getting out of more longs today. I am also positioned on both sides of VIX.

TGT raised full year guidance and it’s shares rallied yesterday. The discount stores are seeing consumer strength, while the home improvement stores (HD, LOW) are seeing weakness. Target CEO Brian Cornell said….

"Consumers have shown remarkable resilience in the face of multiple challenges over the last several years and they remain resilient today. Given the significant headwinds they faced with inflation over the last few years, consumers continue to focus on value as they work hard to manage their household budgets. And while they continue to turn out and shop around holidays and other seasonal moments, many are delaying purchases until the moment of need."

I tend to agree with Mike O’Rourke here…..

The combination of retailer earnings and the Payrolls revisions painted a more nuanced picture of the economic outlook. There was nothing robust about any of the data points received today. The commentary has the impression of consumers barely hanging on. A more discerning view is that of an economy approaching a tipping point, one for which investors should want to be prepared. Nonetheless, that inflection point has not arrived. The September rate cut was already a lock. Despite the persistently hopeful nature of the Fed Funds futures, it would still be a reach to cut more than 25 basis points in an economy that is continuing to grow. The equity market continues to price in the rosiest outlook which is not consistent with the slowdown that is emerging.

Interesting if true: Hedge funds have refrained from investing in the rebound rally, Goldman says-MarketWatch

Hedge funds are now on course to net sell global equities at their fastest pace since March 2022, when markets were hit by Russia’s invasion of Ukraine, Goldman Sachs’ analysis of its prime brokerage data shows.

“Despite the market rebound, gross and net leverage ratios have declined so far in August, suggesting little recovery in risk appetite after the large de-grossing episode in July,” Goldman Sachs analysts, led by Vincent Lin, said in a note.

Imagine AI integrated with every iPhone. Apple Stock Is the Real Bargain in Big Tech. It’s Not What You Think.-Barron's

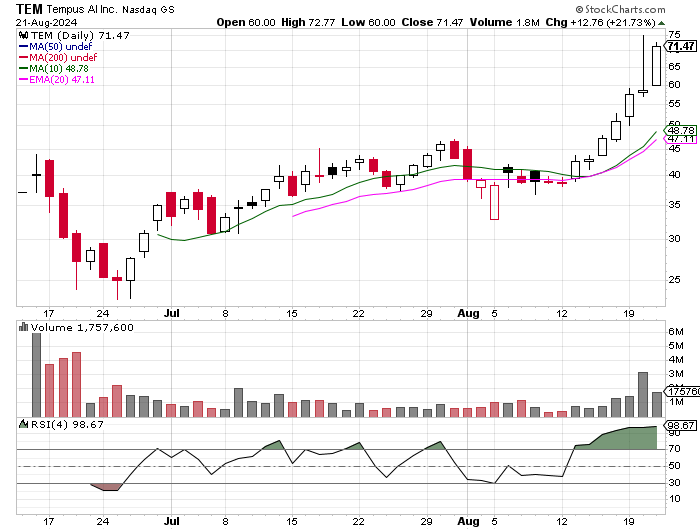

Speaking of AI, keep an eye on TEM (Thank you Larry Connors). Jensen said that digital biology will be the next big thing in AI.

Larry Connors has a great AI report, well worth the subscription price IMHO:

AI Wealth Creation Traders Report