Financial News vs. Noise

More of the same yesterday as the market continues to bleed up. One has to wonder if this is going to get the Fed’s interest at all, or respike inflation. Again, this is a first quarter issue, not a now issue.

@zerohedge: This has been the biggest two-month easing in financial conditions in history, surpassing the announcements of QE1, 2, 3, and so on. The market has priced in 136bps, or 5.5x rate cuts since the start of November.

https://twitter.com/zerohedge/status/1739846854005633255

We did end up adding VIX yesterday and getting out of our puts. Not because I flipped bearish, but it’s due for a bounce. I would suspect we would be back in VXX and/or UVXY puts soon.

We also took some profits on MARA and our GLD. I continue to own MFST and AAPL as those are the least extended Mag 7 names. Not sure why AAPL has been weak, but this could have something to do with it.

Apple Can Restart Watch Sales as U.S. Court Pauses Ban-WSJ

China looks strong this morning, I could look at some of those names if I want to ride that roller coaster. ZIM in shipping also continues to look interesting as it pulls back into support.

Besides that the market is extended and you are unlikely to great good moves anywhere as it just melts up. Situations like MARA can be found, but it’s not easy. We would still love another pullback to be able to do some buying.

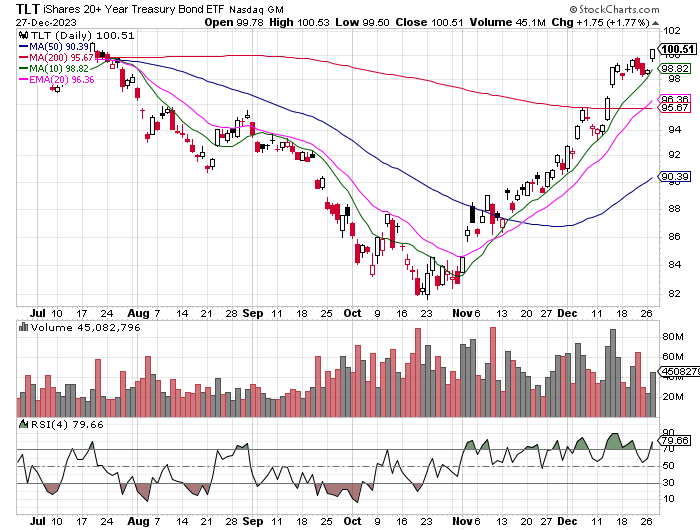

I think we could be nearing a good spot to short TLT. Market is probably pricing in way to many rate cuts and this looks like a meme stock.

This issue has not gone away. We launch SKRE on 1/4, could be half way decent timing. Banking Crisis Plays Out at America’s Smallest Lenders Rural community banks are at risk from giant underwater bond portfolios-WSJ

And these are the kinds of names I would be looking for next year. Weird yes, but you trade the market you have, not the market you want. A record share of S&P 500 stocks have underperformed the index in 2023 as ‘weirdest bull market in decades’ marches on-MarketWatch

Subscribe to our other newsletters

Laffer Tengler Research Bulletin

Matthew Tuttle is the Chief Executive Officer and Chief Investment Officer of Tuttle Capital Management, LLC.

At Tuttle Capital Management (“TCM”), we want to help educate investors about different ways to allocate and manage assets. TCM strives to create innovative portfolio management tools coupled with investment strategies designed to help mitigate risks and potentially enhance returns.

The views and opinions expressed herein are those of the Chief Executive Officer and Portfolio Manager for Tuttle Capital Management (TCM) and are subject to change without notice. The data and information provided is derived from sources deemed to be reliable but we cannot guarantee its accuracy. Investing in securities is subject to risk including the possible loss of principal. Trade notifications are for informational purposes only. TCM offers fully transparent ETFs and provides trade information for all actively managed ETFs. TCM's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. Trade notification files are not provided until full trade execution at the end of a trading day. The time stamp of the email is the time of file upload and not necessarily the exact time of the trades.

Tuttle Capital Management is not a commodity trading advisor and content provided regarding commodity interests is for informational purposes only and should not be construed as a recommendation. Investment recommendations for any securities or product may be made only after a comprehensive suitability review of the investor’s financial situation.

© 2023 Tuttle Capital Management LLC (TCM). TCM is a SEC-Registered Investment Adviser. All rights reserved.