Financial News vs. Noise

Yesterday we launched NSI:

This is an emerging market ETF that excludes companies, specifically in China, that make military hardware or software that can be used against out troops.

We had a sense that Wednesday was a buying opportunity, not a market top. Today we have non farm payrolls. It seems like positioning is extremely bullish coming into this number, which says to me that the risk is to the downside. I have no idea what the number will be, or what reaction to it will be, but I do think yesterday was a day to take some chips off the table and see what today brings. As the market continues to be in an uptrend I would love to buy back into weakness today.

I cut a ton of equity exposure yesterday, but I did add ET in the MLP space. The MLPs are the only area in the oil space above their 200 day moving averages.

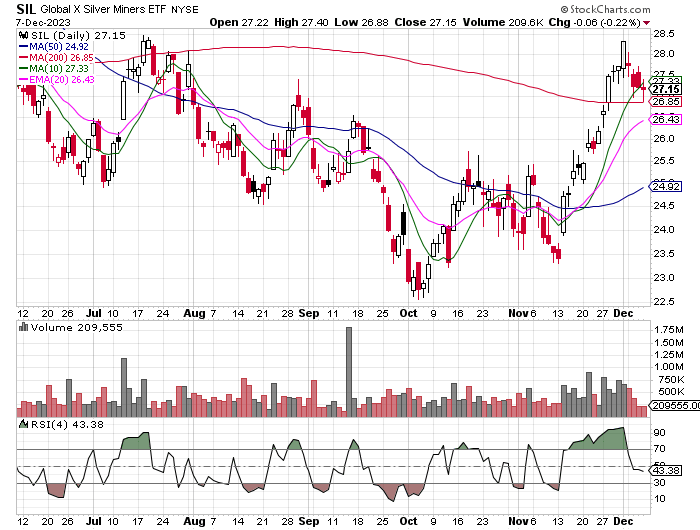

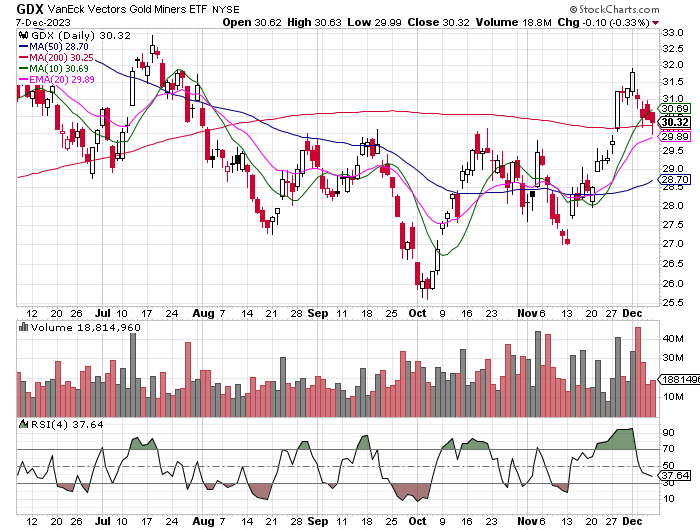

Gold miners undercut and rallied at their 200 day yesterday, while silver miners came close but held.

It is likely the jobs number will move these guys after a dull day yesterday, the question is which direction? We are still long.

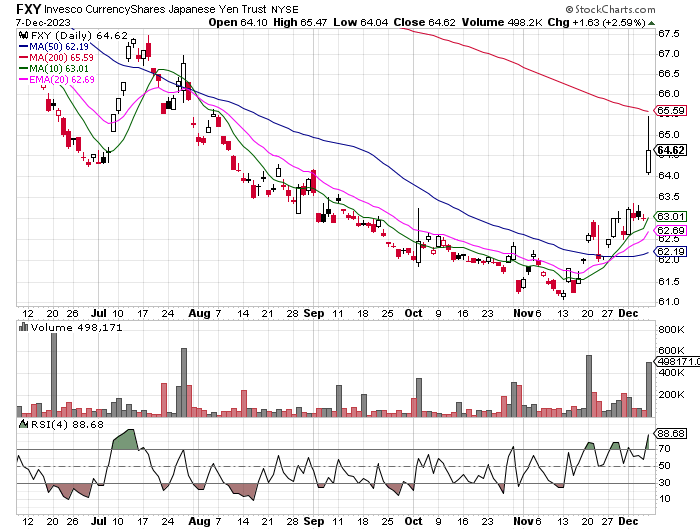

I exited the Yen yesterday but will look to get back in on any weakness.

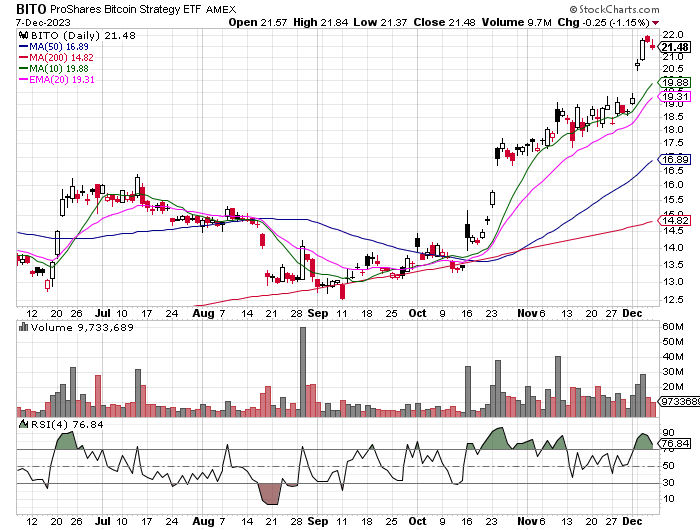

Eyeing Bitcoin here on the long side. Missed the gap up, but it was down yesterday and weak so far this morning. Further weakness today could bring it into buying range for me.

A lot of the retail favorites got crushed yesterday-AI and BYND specifically. GME and CHWY came way off their lows so will see if that sparks anything today. Sentiment around the jobs number is going to impact that a lot.

Volatility has been interesting, well as interesting as dull volatility can be. We have 7 shorter term models to be short volatility and only 1 is still in, just barely. We have four models to be long volatility, 3 are in. So net, net we are long. We have also been watching the implied volatility curve for SPY puts. Up until yesterday we didn’t see much of a difference in implied volatility today and Wednesday (FOMC). Yesterday we finally saw implied vol widen out on those two days. Not sure if that means anything or not, but will be watching.

Mohamed El-Erian wrote an op ed in the Financial Times and issued the following warning:

“the more markets diverge from the Fed’s signals, the more likely they are to push the central bank to adopt the path that is detrimental to them. This is because markets’ affinity for rate cuts loosens financial conditions and heightens the Fed’s concerns about inflationary pressures...”

Again, I think this is next year’s problem, not this year’s, but a hot number today could create some issues.

Marko Kolanovic came out with his year ahead outlook. Not that I care, but other people do:

As we approach 2024, we expect both inflation data and economic demand to soften, as the tailwinds for growth and risk markets are fading. Overall, we are cautious on the performance of risky assets and the broader macro outlook over the next 12 months, due to building monetary headwinds, geopolitical risks and expensive asset valuations.

Subscribe to our other newsletters

Laffer Tengler Research Bulletin

News vs. Noise

As I said above, I think this is going to be a huge problem, just think it’s next year’s problem. Double Trouble: Investors Fight the Fed on Two Fronts Rate expectations have plunged for next year, but further out they are still high-WSJ

Something to keep an eye on. This is what El-Erian is warning about. November’s rally just erased two months of Fed tightening, economist says-MarketWatch

I love it, but I don’t own the stock. Hope he joins one of the Discords I am in. GameStop’s Plan to Trade Equities Is Called ‘Inane’ by Analysts-Barron’s

Matthew Tuttle is the Chief Executive Officer and Chief Investment Officer of Tuttle Capital Management, LLC.

At Tuttle Capital Management (“TCM”), we want to help educate investors about different ways to allocate and manage assets. TCM strives to create innovative portfolio management tools coupled with investment strategies designed to help mitigate risks and potentially enhance returns.

The views and opinions expressed herein are those of the Chief Executive Officer and Portfolio Manager for Tuttle Capital Management (TCM) and are subject to change without notice. The data and information provided is derived from sources deemed to be reliable but we cannot guarantee its accuracy. Investing in securities is subject to risk including the possible loss of principal. Trade notifications are for informational purposes only. TCM offers fully transparent ETFs and provides trade information for all actively managed ETFs. TCM's statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. Trade notification files are not provided until full trade execution at the end of a trading day. The time stamp of the email is the time of file upload and not necessarily the exact time of the trades.

Tuttle Capital Management is not a commodity trading advisor and content provided regarding commodity interests is for informational purposes only and should not be construed as a recommendation. Investment recommendations for any securities or product may be made only after a comprehensive suitability review of the investor’s financial situation.

© 2023 Tuttle Capital Management LLC (TCM). TCM is a SEC-Registered Investment Adviser. All rights reserved.